Our Strategies

- Life Insurance Policy Reviews

- Asset Preservation

- Retain, Recruit, & Reward Key Executives

- Premium Financing

- Executive Retirement Plans For The Highly Compensated

- Retirement Income

- Buy/Sell Funding Arrangements & Key Man Insurance

- Disability Income Replacement

- Charitable Giving

- Private Placement Life Insurance & Annuities

- Long-Term Care

- International Business

- Types of Life Insurance

Life Insurance Policy Reviews

The performance of life insurance policies is almost always different than the original illustration. That is because the variables that drive performance are different than the original assumptions. These variables change over time. Periodic audits and regular policy reviews should be done to avoid surprises (like policy lapses) and help ensure policy efficiency. With our access to proprietary products, we can potentially improve existing policy premiums, death benefits, and cash values.

Largely because of our M Financial proprietary products, we may be able to lower the premium for the same coverage or considerably increase the face amount for the same premium outlay.

Asset Preservation

Retain, Recruit, & Reward Key Executives

The Restricted Bonus Plan is a company sponsored program that enhances the participant’s compensation package. These plans:

- Are provided to a select group of key employees.

- Involve an addition to the participant’s regular compensation.

- Provide the participant with a life insurance policy that should become a valuable part of their overall estate plan and retirement income strategy.

KEY PLAN FEATURES:

Company Contributions

A specified percentage of the participants base compensation will go into the life insurance policy to fund the plan. The participant will own the life insurance policy. The plan will be re-evaluated each year by TMH.

Tax-Free Retirement Income

Tax-free distributions from the insurance policy are intended at age 65 or 70 for 15 to 20 years. Tax-free access to cash is available after vesting. Tax-free death benefit is also provided.

Investment Choices

Each year the participant may select among several indexed strategies. As a safeguard, each index segment has its own investment cap and floor.

Taxes

The participant will receive tax-free distributions from the policy’s cash value. They will also receive a tax-free death benefit.

Vesting Schedules

The company may utilize vesting schedules for those employees where retention is an issue. After vesting, the participant may use the policy at their discretion, although it is intended as a valuable retirement vehicle.

Ownership

The participant will own the policy. Unlike a deferred compensation plan, it is not a corporate asset. The employee does not need to worry about risk of forfeiture due to company bankruptcy.

Death Benefit

If structured properly, the death benefit will be tax-free to the executive’s family.

Premium Financing

Borrowing to pay larger premiums should be considered. It may be a more cost effective way to fund a policy. Depending on interest rates, it may reduce the out of pocket cost of buying a life insurance policy. Individuals that have a need for insurance but don’t want to disrupt current cash flow, lifestyle, and investment opportunities may be able to use a premium finance strategy. The life insurance policy cash value will act as the primary collateral for the loan. In the early years the cash value may not be sufficient to fully collaterize the loan, so a small amount of gap collateral will need to be posted.

Common methods to finance premiums are bank borrowings, company borrowings, and investment account margin loans. Life insurance IRR’s may be increased using premium finance.

We have establised relationships with several large banks that specialize in premium finance. TMH can help negotiate competitive arrangements.

Executive Retirement Plans For The Highly Compensated

The Deferred Compensation Plan offers you a tax-favored savings opportunity. You can:

- Defer more pre-tax compensation than a 401(k) plan.

- Postpone income taxes on your deferrals and returns.

- Schedule penalty-free withdrawals while still employed to meet short-term goals.

- Contribute to a financially sound retirement in a tax-effective manner.

KEY PLAN FEATURES:

Deferrals

You may defer 3% to 80% of your annual base salary; from 5% to 100% of your incentive compensation; and up to 100% of additional cash or restricted stock compensation. Your deferrals and their returns are always fully vested.

Distribution Options

You may select a separate distribution for each year’s deferral balance. You may schedule in-service withdrawals, payable in a lump sum or annual installments over 5, 10, 15, or 20 years.

Investment Choices

You may choose from a variety of deemed investment crediting options in a broad range of asset classes.

Taxes

Deferrals and returns are not subject to income tax until paid out to the participant.

Corporate Accounting

The corporate tax deduction is deferred until the benefit is paid. The plan needs to comply with IRC 409A.

Retirement Income

Properly structured, significant tax-free retirement income may be available from a life insurance policy. A significant death benefit is also available for the family. Life insurance is often viewed as an interesting investment alternative. Investment professionals focus on the insurance policy IRR’s and view this asset class as a very important part of their investment portfolio.

Additional key features include the ability to make larger contributions than traditional qualified plan accounts. Individuals may access the cash value without penalty.

Loans and partial withdrawals will decrease the death benefit and cash value and may be subject to policy limitations and income tax. Diversification does not ensure a profit or protect against loss in a declining market.

Companies with two or more owners should have buy/sell agreements in place for owners to fund the purchase of stock of a deceased owner. Life insurance is typically used to fund this obligation.

Is your business prepared to continue if a crisis happens to you or one of your partners? Would you want a deceased partner’s spouse to take their place in the company? Anyone who has one or more partners should have a funded buy/sell agreement with a current valuation.

There are four different ways to structure a buy/sell agreement depending on your situation:

- Trusteed cross purchase

- Entity purchase agreements

- Cross purchase agreements

- Wait and see agreements

KEY MAN INSURANCE

Replacing a key person can be difficult, expensive, and time consuming for a company. Key man life insurance is an important way to replace lost revenue if a key person dies. Inexpensive term insurance can be a great solution.

Disability Income Replacement

One of the largest providers of supplemental disability income insurance is UNUM. UNUM provides a proprietary product for M Member Firms. One of the key features is a larger discount for multi-life programs.

TMH has access to other non-M disability providers such as Mass Mutual, Guardian, and Lloyd’s of London. Some of the high-limit coverages include:

- Individual Disability, Key Man, Buy/Sell

- Interim Life Coverage to Protect a Third Party Contractual Obligation (Failure to Survive)

- Accident Coverage- Life Exclusion Buy-Back Programs, Business or Personal Travel, Events

- War & Terrorism, Kidnap & Ransom

- Experience Available for Entertainer/Athlete Markets

Charitable Giving

Many wealthy individuals are charitably inclined. Life insurance may be a way for these donors to complete their expected lifetime gifts should they die prematurely.

The primary ways to make a charitable gift are:

- Naming the donor as owner and the charity as beneficiary of the life insurance policy

- The donor transfers ownership of an existing policy to the charity

Any tax benefits to the donor will vary depending on how the gift to the charity is structured. If the donor maintains ownership, names the charity as the beneficiary, and does not take a current tax deduction for the current premiums, there will be a reduction in their taxable estate by the amount of the death benefit paid to the charity. Premium financing may also be used as an effective strategy. TMH can assist in educating the donor regarding the alternatives.

Private Placement Life Insurance & Annuities

Ultra-affluent families utilize Private Placement Life Insurance and Annuity Investment Accounts to shield traditional and alternative asset class investments from current period taxation. These accounts can increase after-tax investment returns, eliminate K-1s, enhance creditor protection, increase charitable bequests, reduce the reporting requirements for foreign financial institutions, and/or shield foreign wealth from U.S. income tax.

Private placement insurance products occupy a unique place in the spectrum of financial products. While having the same tax benefits, private placement insurance products offer policy structures and investment alternatives not found in traditional variable universal life (VUL) and variable annuity (VA) products. Because they can only be offered to individuals who are qualified purchasers and accredited investors*, private placement variable universal life (PPVUL) and variable annuities (PPVA) offer high net worth clients access to both investment alternatives and customized product designs that are difficult or impossible to obtain in traditional registered products. They are well suited in their use as a tool to address a multitude of financial, income, and estate planning objectives. However, the life insurance death benefit is typically a secondary consideration. Because of its preferential treatment from an income tax perspective, the insurance policy must be properly structured in order to assure it maintains its tax benefits.

Investment Options- variable insurance contracts are permitted to invest in segregated asset accounts. These accounts are required to be diversified such that no single asset may comprise more than 55 percent of the value of the account. Further, the investment accounts available to a variable insurance contract should only be open to investments from insurance contracts and not be co-mingled with non-insurance investments.

In addition, the “investor control” doctrine requires that holders of variable insurance contracts not have control over segregated account assets sufficient to be deemed the owner of the assets. If the policyowner is deemed by the IRS to exercise control of the segregated account, the policy will be disqualified as insurance for tax purposes.

Private Placement Life Insurance is an unregistered securities product and is not subject to the same regulatory requirements as registered variable products. As such, Private Placement Life Insurance (or Annuities) should only be presented to accredited investors* or qualified purchasers as described by the Securities Act of 1933.

*Accredited Investors are individuals having a net worth exceeding $1,000,000 or an annual income of over $200,000 for the last 2 years. Qualified Purchasers are individuals with a minimum of $5,000,000 of investable assets.

Long-Term Care

The long term care market has dramatically changed in recent years and has become increasingly more expensive. A popular long term planning solution is now using a life insurance policy to provide for long term care benefits. TMH can assist in navigating through the various options.

International Business

Wealthy individuals who travel extensively and have meaningful economic ties to the United States may have a need for life insurance coverage to safeguard their financial interests at home and abroad. TMH can help these individuals meet their personal, business, retirement, and wealth transfer objectives. Many countries have severely limited domestic capacity for life insurance and even in countries without estate taxes, individuals often look to non-domestic options to meet business/estate planning needs. The number of underwriting classes is limited to just a few classes in many countries and policyholder protection (e.g., regulations limiting contestability) is much less onerous to carriers. Products available outside the U.S. are often viewed by buyers, carriers, and the reinsurance market as much less competitive than products available in the U.S. high net worth market, particularly in M proprietary product.

WHAT DEFINES A WEALTHY GLOBAL CITIZEN? (FOR LIFE INSURANCE PURPOSES)

A wealthy global citizen is someone with a high net worth (over U.S. $2.5 million) and high income (over U.S. $250,000 per year) who meets one of these criteria:

- A non-U.S. citizen with foreign residence or long-term foreign travel

- An individual residing in the U.S. without permanent resident qualifications

- A U.S. citizen or permanent resident who travels to a foreign country more than 12 weeks each year

Examples:

- Foreign nationals with established U.S. ties

- Expatriates living overseas

- Global companies with cross-border employees

- Affluent foreign nationals living abroad, with no or minimal U.S. ties

- Affluent U.S. citizens or foreign nationals with a unique need for offshore solutions and alternative investments

- Foreign nationals moving to the U.S. temporarily with pre-immigration planning needs

INTERNATIONAL MARKETPLACE

High net worth, global citizens build their wealth across multiple borders by establishing international connections through businesses, families, properties, and investments. While international borders no longer confine global citizens of the world today, they can still require sophisticated financial planning and exceptional product solutions. International insurance products often provide unique planning solutions for the challenging issues confronting global citizens.

Basic Planning Needs

Global clients have basic planning needs that address sophisticated business and family structures:

- Income Replacement

- Survivor Income and Liquidity

- Creditor Protection

- Estate Planning

- Business Continuity

- Executive Retention and Compensation

- Asset Preservation

Unique Challenges

Global clients often have unique challenges that arise from cross-border issues or country of residence restrictions:

- Forced Heirship Laws

- Sovereign Risk

- Inflation Protection

- Global Family Inheritance

- Ownership of Cross-Border Businesses

- Corporate Benefits for Cross-Border Employees

- Multinational Tax Liabilities

- Limited Access to Insurance Capacity and Product Selection

ADVANTAGES OF THE U.S. LIFE INSURANCE MARKET FOR INTERNATIONAL CLIENTS

Affluent individuals with citizenship and assets in multiple countries often have complex planning needs and must frequently consider the jurisdiction where their assets are held. Due to the importance of life insurance in many estate and business planning transactions, the jurisdiction where the policy is purchased can greatly impact the outcome. For international families with connections to the United States, U.S. domestic life insurance products provide a number of key advantages over products available outside the U.S. market.

Legal Structure

Sovereign risk, or the risk of drastic regime change or governmental collapse, is a significant concern for affluent individuals with multi-jurisdictional planning needs. The U.S. offers global investors one of the lowest levels of sovereign risk in the world. The legal system in the U.S. offers relative predictability and transparency; legal processes are generally well-defined, and relatively free from bias or outside influence. As a life insurance policy is a contract between the insurer and policy owner, the well-established field of contract law determines disputes with generally predictable outcomes.

U.S. life insurance taxation is well-defined in the U.S. markets and provides a number of favorable tax treatments to policy owners. A properly structured U.S. life insurance policy can accumulate cash value on a tax-deferred basis. Gains within the policy can be accessed through tax-free loans and withdrawals, and the death benefit can be received income tax free. Loans and partial withdrawls will decrease the death benefit and cash value and may be subject to policy limitations, income tax, and includes the potential for policy lapse. These tax treatments may not be available in all jurisdictions.

The legal structure surrounding U.S. life insurance transactions also affords a relatively high degree of confidentiality and privacy that is unavailable in many other countries.

Insurance Carrier Environment *

The U.S. life insurance market is the world’s leading premium-writing country, with a wide variety of substantial competitors. The first life insurance company in America—Presbyterian Ministers Fund for Life Insurance—was chartered in 1759, seven years prior to the nation’s Declaration of Independence in 1776. Today, more than 850 U.S. companies are in the industry.

The U.S. life insurance industry is highly regulated, with oversight from multiple state and federal agencies. The primary source for regulation occurs at the state level—each state’s insurance commissioner has the authority to license insurance companies and agents in their jurisdiction. The National Association of Insurance Commissioners (NAIC) was founded in 1871 and consists of insurance commissioners from all 50 states. The NAIC promulgates model regulations and laws for the industry, which are generally adopted by the state commissioners.

In addition to state regulation, some oversight exists at the federal level. The Securities and Exchange Commission (SEC) regulates the sale of variable life insurance and annuities as securities, and therefore requires compliance with its regulations for companies and agents offering these products. In addition, the Financial Industry Regulatory Authority (FINRA) is a self-regulating organization that is overseen by the SEC and is responsible for enforcing rules for its members. As a result, the U.S. life insurance industry is subject to a wide variety of licensure, product, suitability, and solvency regulation, creating a stable environment for insurance purchasers and policyholders that doesn’t exist in many other international jurisdictions.

U.S. life insurance companies also generally subscribe to independent financial ratings agencies, such as Moody’s, A.M. Best, Standard & Poor’s, and Fitch Ratings. These agencies asses the financial and operational status of participating insurance companies and provide insight into the financial quality of insurers, as well as the quality and liquidity of their underlying assets.

The dollar denominated nature of U.S. life insurance products increases their attractiveness to foreign buyers, as the currency is subject to a lower degree of inflation volatility and default risk than many other currencies, especially in smaller jurisdictions.

Product and Operational Advantages

The U.S. industry’s scale, duration, and competitive structure has resulted in a wide variety of price-efficient and effective product offerings for affluent individuals. As insurance products rely upon the pooling of risks, a more thorough understanding of risks leads to more transparent and competitive pricing. The thorough understanding of mortality rates in the U.S., along with improvements in mortality in recent decades, has led to lower mortality charges in U.S. life insurance products as compared to other international jurisdictions.

The competitive nature of the U.S. life insurance industry leads to an increased motivation for insurance carriers to pursue product innovation and bring competitive new offerings to the market. Many U.S. life insurance products offer sophisticated and innovative features that are not found in other markets.

The underwriting process, where risks are assessed and categorized by insurers, is well-defined, with sophisticated knowledge and procedures, allowing U.S. life insurers the ability to efficiently and appropriately price risks. This leads to better product pricing for clients and the potential for better performing in-force policies. In addition, U.S. life insurance companies are global leaders in implementing technology-based solutions that enhance the underwriting process.

The U.S. life insurance market offers purchasers and policyholders well-developed, in-force policy service standards, claims payment processes, and dispute resolution options. Eligibility requirements for U.S. products vary across carriers, but often include a combination of financial and physical presence in the U.S.

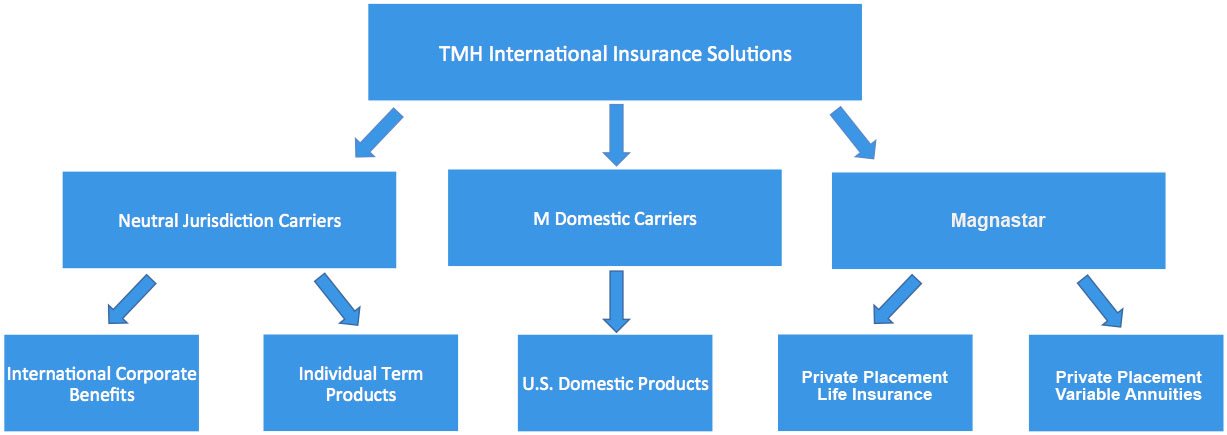

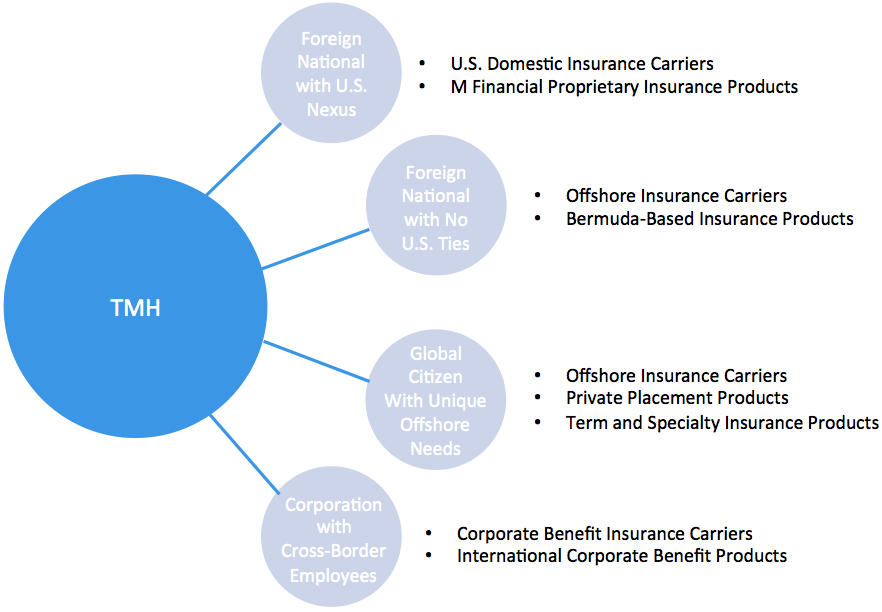

TMH INTERNATIONAL PLATFORM

As part of M Financial, TMH has established an international platform that provides access to U.S. and offshore insurance products with global client support across five different segments of international insurance solutions:

TMH INTERNATIONAL SUPPORT

It takes international experience, access to U.S., and offshore carrier products, and ongoing resources for support and coordination to meet the current and future cross border needs of global clients.

| DESCRIPTION | OPTIONS | |

| FOREIGN NATIONAL CLIENT WITH U.S. NEXUS |

|

|

|

FOREIGN NATIONAL CLIENT WITH NO U.S. TIES |

|

|

|

GLOBAL CITIZEN WITH UNIQUE OFFSHORE NEEDS |

|

|

|

CORPORATION WITH CROSS-BORDER EMPLOYEES |

|

|

Payment of death benefits and the processing of surrenders and withdrawals will be subject to all applicable tax laws and treaties.

Types of Life Insurance

- Term life insurance: temporary, providing coverage for a set period of time.

- Cash value life insurance: can provide permanent coverage and involves an internal savings component.

TERM LIFE INSURANCE

Term life insurance pays a specified face amount (i.e., death benefit) if the insured dies during the policy term. The policy term is usually specified as a number of years, such as 10 or 20, or to a specified age, such as age 65. If the insured outlives the specified period, the term life insurance contract expires, usually with no residual value. Term insurance has no cash value.

Premiums for most term contracts are fixed and guaranteed at issue. The majority of term contracts provide level death benefit coverage, although decreasing and increasing death benefit coverage is available as well.

There are two types of term policies:

- Renewable Term: the term policy’s annual premium increases with the insured’s age.

- Level Term: the term policy’s annual premium remains the same throughout the level term period.

Term policies with increasing premiums are called renewable. Renewable term insurance provides coverage for a stated number of years and allows the policy owner to renew the policy for the successive periods without furnishing evidence of insurability. Yearly renewable term (YRT) features premiums that increase annually. Other term policies have increasing premiums on a basis of three, five, or ten years— three-year renewable term, five-year renewable term, and ten-year renewable term. The right to renew is usually limited to a stated number of years or up to a specified age.

Level term policies have premiums that remain the same each year. Level term policies are typically used to cover a certain number of years—10-year and 20-year term are most common. Some level term policies may have the ability to be renewed (i.e., become a YRT contract) after the specified number of years have passed.

A variation of level term provides coverage intended to last an employee’s typical working life, but is not renewable. These contracts include life-expectancy term and term-to-age 65, and are rarely sold.

Another variation of traditional level term insurance is return of premium (ROP) term insurance. ROP term insurance returns all premiums if the insured survives to the end of the specified term period. ROP insurance is considerably more expensive than traditional term insurance.

Re-entry term insurance allows the policy owner to pay a lower premium at the time of renewal if he or she meets certain insurability criteria. If the insured does not re-qualify, the rates remain at the guaranteed level, which are much higher than the re-entry rates.

Many term insurance policies include a convertibility provision. Convertibility allows a policy owner to replace term coverage with permanent coverage, within a specified period, without evidence of insurability. Convertibility provisions allow the policy owner to obtain term insurance, or temporary coverage, and reserve the option to purchase permanent coverage for an amount equal to the term insurance face amount if needs change. Conversion typically must occur within a specified number of years no greater than the length of the term period.

CASH VALUE LIFE INSURANCE

Cash value life insurance, also referred to as permanent coverage, differs from term because the premiums paid are sufficient to cover the death claims and expenses of the insurer and also build a cash value, or savings fund, within the contract. The permanent life insurance variations described below are whole life insurance, universal life insurance (UL), indexed universal life insurance (IUL), variable universal life insurance (VUL), and no-lapse guarantee life insurance (NLG).

Whole Life Insurance

A whole life insurance policy’s face amount will be paid at the death of the insured, no matter when the death occurs, as long as the policy is in force. The policy owner must pay the scheduled premiums on time and meet the requirements of the policy to keep the policy in force.

Premiums for most whole life insurance contracts remain level and are calculated to ensure that the policy will remain in force for the lifetime of the insured (i.e. age 121). The initial annual premiums can be several times higher than those of a term policy with a comparable face amount. These higher premiums fund the permanent coverage while establishing cash values within the policy. The cash value forms a reserve, enabling the insurance company to keep premiums level and still pay the policy’s full death benefit. Policy owners may borrow from cash values via policy loans pursuant to the terms and conditions of the contract. Optional riders and benefits, in addition to the policy death benefit, may be added to the policy.

Whole life insurance policies can be issued as participating or nonparticipating. Participating policies are entitled to share, via non-guaranteed policy dividends, in any distribution of the insurer’s surplus funds that it decides to make to those policies. Nonparticipating policies are not entitled to dividends.

Universal Life Insurance

UL policies offer more flexibility and transparency relative to whole life policies. The policy owner has the ability to modify the amount and duration of premium payments, within certain limits, and still maintain coverage for life as long as the cash value reserve is positive.

UL premiums, which are typically made annually, are reduced by the current policy expenses and the remainder is deposited into the cash value account of the policy. Each month, the cash value is credited with interest and the policy is debited by a cost of insurance (COI) charge and any other policy charges and fees drawn from the cash value. Interest credited to the account is determined by the insurer (in the form of a crediting rate) and may have a contractually guaranteed minimum rate.

Death benefits in a UL contract may be fixed at a specified level or may increase each year by an amount equal to either the accumulated cash value or the premiums paid. Similar to whole life contracts, loans may be taken out against the cash value and riders may be added.

Indexed Universal Life Insurance

IUL is a UL variation with the same operational characteristics and platform, but with an interest crediting rate determined by reference to an equity index, such as the S&P 500 without dividends. The index return is typically adjusted by a participation percentage rate, then subject to a maximum interest rate cap and minimum interest rate floor. IUL offers the potential for a higher yield than UL, with indirect participation in the equity market, as well as a guaranteed minimum crediting rate (i.e., floor) that provides downside protection for the policy owner.

Variable Universal Life Insurance

VUL insurance policies are also based on the UL platform, varying in their investment flexibility and risk/return opportunity. VUL products permit the policy owner to allocate a portion of each premium payment into one or more “separate account” funds. Separate accounts, which are similar to mutual funds, are not subject to the restrictions of the carrier’s general account portfolio, reducing the policy owner’s exposure in the event of carrier insolvency.

VUL policies are monitored and subject to the rules established by the Securities and Exchange Commission (SEC), as the investment options are deemed to be securities. All VUL policies must be accompanied by a prospectus that provides detailed information on policy mechanics, policy expenses and changes, and general information regarding the inherent risks associated with securities.

VUL is most appropriate for individuals willing to accept greater risk for greater reward, as the policy’s cash value is dependent on non-guaranteed market value changes.

No-Lapse Guarantee Universal Life Insurance

NLG life insurance policies are UL policies with a guarantee that if a specified minimum premium is paid regularly, the policy will not lapse for a specified period, or for life, even if the cash value decreases to zero.

NLG insurance is often characterized as having minimal or no cash value accumulation. It is best suited for individuals focused on ensuring the life insurance death benefit will be available at a guaranteed cost, and where cash value accumulation may be less important.

NLG may also be offered as a rider on other forms of life insurance, including VUL and IUL. In some instances, the duration of the NLG policy may be contractually fixed by the insurance carrier. In contrast to a pure NLG insurance policy, NLG riders may be available on products where cash value accumulation is a key benefit of the policy. These types of contracts can serve the dual purpose of providing cash value accumulation, and a death benefit that is contractually guaranteed, as long as the policy owner meets certain requirements.

SUMMARY

Life insurance serves a wide variety of purposes, providing financial support to heirs and charitable organizations, indemnification against the loss of a key person of a business, funding of a business continuation plan, and as a benefit for executives and employees. Between the two basic types of life insurance, term and cash value (Appendix A summarizes the characteristics of each), there is a solution for a wide range of planning needs and objectives.

Appendix A: Term and Cash Value Life Insurance Comparison

|

TERM LIFE INSURANCE |

CASH VALUE LIFE INSURANCE |

|||||

| ATTRIBUTE |

N/A |

WHOLE LIFE |

UL |

IUL |

VUL |

NLG |

| ACCUMULATES CASH VALUE |

No |

Yes |

Yes |

Yes |

Yes |

Yes |

| COVERAGE DURATION |

Fixed |

Life |

Flexible |

Flexible |

Flexible |

Flexible |

| PREMIUM FLEXIBILITY |

No |

No |

Yes |

Yes |

Yes |

Yes, but will impact NLG |

| GUARANTEED ELEMENTS |

Death Benefit and Premium |

Death Benefit, maximum premium, and minimum cash values |

Death Benefit, maximum charges, and minimum interest crediting rate |

Death Benefit, maximum charges, and minimum interest crediting rate |

Maximum charges |

Death Benefit, premium, maximum charges, and minimum interest crediting rate |

| NON-GUARANTEED ELEMENTS |

None |

Dividends |

Current interest credits and charges |

Equity index changes and current charges |

Market value changes and current charges |

Current interest credits and charges for cash values |

| PRIMARY APPEAL |

Guaranteed coverage for a specific period and low premium outlay |

Guaranteed lifetime coverage, backed by investments made by the issuer |

Flexibility, transparency, and backed by conservative investments |

Flexibility, transparency, and limited equity-like returns in return for a guaranteed floor |

Flexibility, transparency, and mutual fund returns |

Guaranteed lifetime coverage at a potentially low premium outlay |

| M PROPRIETARY PRODUCT |

Yes |

No |

Yes |

Yes |

Yes |

Yes |